Many articles have been written on oil price determination. Other than going into the price dynamics this article will investigate deeper the typical commodity oil price drivers and what makes it price determination different than other commodities, like for example gold.

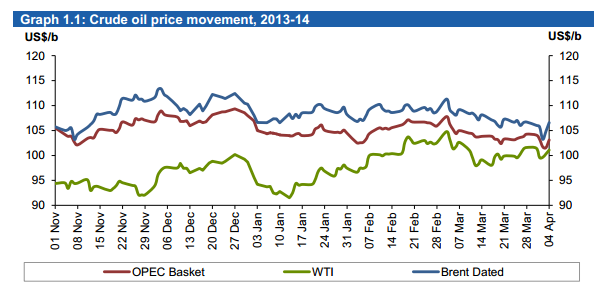

OPEC reports on last oil prices (April 2014 Monthly Oil Market Report) state that the oil price goes slightly down due to slowing pace of economic growth in China, lower refinery demand and ample supply.

Source: OPEC MOMR April 2014

Classical economic theory state that the price on the market is determined where supply meets demand. When demand goes up, ceteris paribus (supply stays equal), prices will go up. On Investopedia it is already commented that in reality this does certainly not always have to be the case for the oil market. Why not? This is because most of the oil is traded in futures. A future contract gives a buyer the right to buy a commodity against a price determined at the moment the trade is made.

Future oil prices are then determined in the contract as expectation to what oil prices will be or the amount the buyer is willing to hedge for. The key points which are being made in the article is that rather than supply, demand and sentiment, future supply, demand and sentiment are the underlying factors which determine the oil price.

To go deeper into the price dynamics of oil we will first take a closer look at an ‘easier’ commodity like gold. The value of gold is mainly set by the appreciation and worth we adhere to gold. Other than industrial and practical uses of gold, there is a demand for gold because of its appealing. This demand for the appeal of gold has been relatively constant. Prices of the commodity of gold do change. Gold is commonly described as anti-cyclic product. This means that prices become higher when the economy enters a crisis (When other investment opportunities are lower) and prices become lower when the economy is booming. Investors find a safe haven in trading in gold in times of crisis, because we expect the demand for gold to be there, also in the future.

The expectation to what oil prices will do in the future is harder to assess. Oil can be cyclic as well as anti-cyclic. Anti-cyclic because oil can also be a safe haven investment, but also cyclic because when economy is doing well, this generally pushes up oil demand – think for example of more trade and transport, car use and industry growth.

– For short term supply and demand variations for oil can be predicted quite well. This can be factors like the economy of China which shows less promising results, combined with a temporary over supply.

– For longer term this is more difficult to determine. 1) The oil quantity is limited and 2) innovations in sustainable energy are being made.

Does this mean that oil prices will go up over time because we are running out? The answer does not have to be yes. It depends on point 2. Two scenarios will illustrate this:

Example a – the slow transition) If over time the oil quantities will diminish and the costs for finding and drilling oil will go up, this will also reflect in the price of oil. This will continue to do so, if ceteris paribus, demand will stay equal or rise (as expected globally). Prices for oil, gas, and electricity will rise, creating eventually a situation where sustainables like solar, wind and others will reach market parity. This means that the cost price of the electricity generated sustainables will be equal or even lower than oil/gas generated electricity.

Example b – the fast transition) the sustainable market will continue to grow strongly, more investments will be made and strong innovations will be made, so that the energy market will start changing rapidly.

For example, currently Tesla Motorgroup is investing 5b USD in the largest battery plant in the world. Imagine that in the next 5 years they will achieve to get electric cars to drive 100% more distance on 1 battery. Imagine next to it, that recent innovations on super charging mobile phones will be extended and improved for car batteries; we will face cars which can drive more than 1000 km on a 10 min. electric charge. At this point, especially in countries where there are large discrepancies between electricity and gasoline/diesel prices (EU), a massive transition will start taking place which will eventually also arrive in the Middle East, Because of more efficient conversion ratios of electric cars, this will then have a demand-driven negative effect on oil prices.

On the other hand, gas might become a more valuable commodity if our energy market will be based more and more on sustainables. Because gas power plants are relatively easy to turn on and off, they might become extremely valuable as back-up electricity generation on days when sustainable energy production is low (cloudy days with no wind, low tidal and wave energy).

The question is to what extend these kinds of scenario analyses are incorporated in the price of oil. To what extend the price is determined by demand-supply dynamics, market experts and buyers who seek for a solid investment or are after hedging, needs additional research. What I do expect with increasing dynamics in the ongoing and accelerating energy transition is that we are going to face increasing volatility in the oil and gas market. For oil companies and oil exporting countries my advice will therefore be to also hedge in their portfolio of oil and gas and invest in other substitutes as well to minimize exposure to the swings of the market.

Ralf Klein Breteler was formerly energy consultant in the Netherlands at a specialized consultancy firm which covers the entire span and value chain of the energy market. He now lives and works in the Middle East where amongst others he shares his vision on the Middle East Energy Markets.